Current Landscape of Carbon Dioxide Removal (CDR) in the Middle East

A regional snapshot: who’s doing what, what’s missing, and why it matters.

Note: The series particularly focuses on the Gulf countries. This is the first article of this series. Click the link below for the series introduction.

Introduction

Carbon dioxide removal (CDR) has become a critical component of global climate strategies. This has led to the emergence of a new climate sector, with both engineered and nature-based solutions under development and early deployment around the world. The Middle East stands at a paradoxical crossroads in this emerging landscape. As a region historically dependent on hydrocarbons, it faces climate risk, while possesses unique advantages that could enable global leadership in carbon removal: abundant renewable energy, essential for powering energy-intensive CDR technologies like DAC; a massive industrial footprint, including cement, steel, and petrochemical facilities that produce waste streams ideal for carbon mineralization. Moreover, the region’s hydrocarbon infrastructure—from CO₂ transport networks to geological formations—can be repurposed to support large-scale carbon storage and deployment logistics.

Globally, other climate practitioners are moving fast. The EU is drafting a Carbon Removal Certification Framework. Companies like Microsoft and Stripe have committed over $1 billion to purchasing high-quality CDR. In China, Tencent has launched its carbon removal accelerator.

Despite clear advantages, carbon removal in the Middle East remains nascent. Pioneering efforts like Oman-based 44.01’s in-situ mineralization have gained global recognition, but most countries in the region lack dedicated CDR policies, investment vehicles, or monitoring frameworks.

This article maps the current landscape of CDR in the Middle East: who’s doing what, what’s still missing, and what it will take for the region to move from potential to leadership.

What is Carbon Dioxide Removal (CDR)

CDR refers to a suite of technologies and practices that extract CO₂ from the atmosphere and store it durably—helping to counterbalance residual emissions and reach net-zero targets. According to the IPCC, the State of CDR report, Carbon Gap, and CDR.fyi, CDR methods can be broadly categorized in two complementary ways:

By Approach:

Nature-based: leveraging ecosystems (e.g., afforestation, soil carbon, blue carbon)

Engineered: using technology to capture and store CO₂ (e.g., DAC, mineralization, BECCS)

By Scientific Mechanism:

Biological: using photosynthesis-driven processes (e.g., biomass growth, soil storage)

Geochemical: using mineral or ocean chemistry to convert CO₂ into stable forms (e.g., enhanced weathering, ocean alkalinity enhancement)

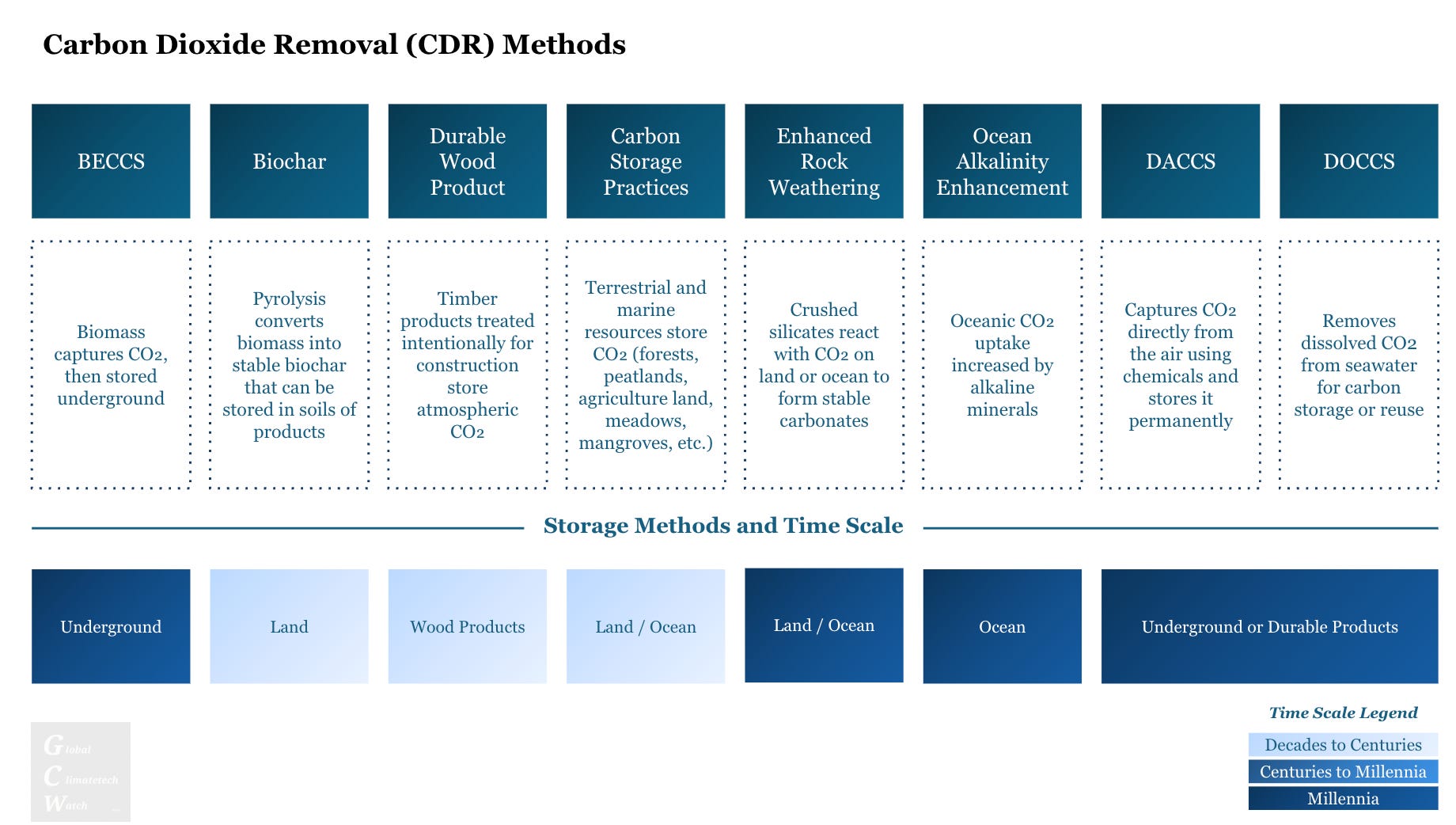

There are multiple CDR methods with diffrerent removal timescale, but in this series, we focus specifically on durable CDR: approaches that ensure carbon stays out of the atmosphere for centuries to millennia.

The chart below presents an overview of key durable CDR pathways (non-exhaustive). It summarizes their underlying mechanisms, storage pathways (e.g., underground, ocean, or in long-lived products), and the permanence of carbon storage time scale—ranging from decades to millennia.

These methods include:

BECCS (Bioenergy with Carbon Capture and Storage)

BECCS combines energy production, biological carbon removal and geological storage. It uses biomass in combustion to generate energy, then captures the emitted carbon for geologic injection. IPCC 2050 projections show BECCS contributing 0.5-5 GtCO₂ removal annually

Example suppliers: Drax, Stockholm Exergi

Cost: $15-$400/t

Regulation & Incentive:

US the Renewable Fuel Standard and the California Low Carbon Fuel Standard both provide tax credits

UK the Industrial Strategy Challenge Fund is supporting the development of these facilities in the industrial clusters

Biochar

Biochar uses biological carbon removal. When biomass and other organic materials are burned in a low oxygen environment, a process called pyrolysis, the carbon inside the biomass transforms to a state where it cannot decay - known as biochar. It is then spread over soil or buried to store carbon in the land. Biochar is projected to remove 2-4 GtCO₂ annually by 2050 according to the IPCC

Example suppliers: Carbo Culture, Carbofex, Carbonfuture, Echo2, Ecoera, Freres Biochar, Husk, Net Zero, Oregon Biochar, Planboo, and Takachar

Cost: $100-$590/t

Regulation & Incentive:

US the Biomass Crop Assistance Program and Conservation Stewardship Program in the USDA Farm Bill provide financial and policy incentives for biochar

UK the GGR-A and GGR-D programmes fund R&D into Biochar utilisation

EU the Sustainable Carbon Cycles regulation

Durable Wood Products

Wood in construction is permanent storage of land based biological removal. Biomass that is processed and treated for construction purposes can permanently store carbon. Cross-laminated timber, laminated veneer lumber (LVL) and glue-laminated timber (glulam) are all timber products that have been treated intentionally for construction and exemplify the removal potential

Example suppliers: Are Treindustrier, BamCore, Ekovilla, Finnish Log House, LapWall, Moelven Limtre, Termowood and TEWO

Carbon Storage Practices (with long-term potential), non-exhaustive

Coastal Blue Carbon (e.g., mangroves, seagrasses, salt marshes): CO₂ is sequestered in anoxic sediments beneath mangrove forests, where organic matter decomposes slowly and is buried under layers of sediment, potentially locking carbon away for centuries to millennia

Example: Abu Dhabi Mangrove Carbon Project (UAE)

Cost: $10-80/t

Enhanced Rock Weathering

Enhanced weathering, or enhanced mineralization, removes atmospheric carbon geochemically. Weathering is a naturally occurring process that converts 1 billion tons of CO₂ into minerals annually. Enhancing this process through human intervention can accelerate the rate of carbon removal. Silicate rocks, such as basalt and olivine, are mined, then undergo a grinding process to form a powder that is spread over large areas of soil. This powder reacts with atmospheric CO₂ to form stable carbonate minerals which permanently store the carbon. By 2050 enhanced weathering could remove 2-4 GtCO₂ annually. When this process takes place in marine environments it is known as ocean alkalinity enhancements, another CDR method

Example suppliers: Aspiring Materials, CO₂ Zero, Cquestr8, Eion, Future Forest Company, GreenSand, Project Vesta and RockFarm

Cost: $75-$500/t

Ocean Alkalinity Enhancement

Ocean alkalinity enhancement is a chemical removal method similar to Enhanced Weathering but in marine ecosystems. Mined and ground silicate rocks, such as basalt and olivine, are spread at the ocean surface, or deposited on beaches and coastal seabeds, where it reacts with CO₂ in the water and in the air to create stable bicarbonates that store carbon permanently. A positive feedback loop is initiated and carbon is further removed by these bicarbonates

Example suppliers: Captura, Ebb Carbon, Heimdal, Planetary Hydrogen, Project Vesta, SeaChange and Solid Carbon

Cost: $1000-$2000/t

DACCS (Direct Air Capture with Storage)

Direct Air Capture and Carbon Storage removes carbon via geochemical processes and geologic storage. Ambient air is passed through either a solid sorbent or a liquid solvent where the carbon bonds with the material and is fixed. When the sorbent or solvent is heated the bonded carbon is released and directed to permanent storage, either via geologic injection or mineralisation. The carbon captured is pure CO₂ that can then be used in products. Currently 0.1MtCO₂ is removed by DAC annually but this is expected to increase to 0.5-5GtCO₂ per year by 2050

Example suppliers: Carbon Engineering, CarbonCapture, Carbyon, Climeworks, Global Thermostat, Heirloom, Mission Zero, Noya, Sustaera and Verdox

Cost: $300-1500, although some projections show this will fall to about $100 per tonne by 2030

Regulation & Incentive:

UK the DAC and GGR Innovation Fund is helping to catalyse start-ups.

US, DAC projects can utilise the 45Q tax credit for $50/t removed (on projects over 100,000 tonnes removed per year) and the Low Carbon Fuel Standard credit at $200/t removed. The 2021 Infrastructure Bill announced the creation of 4 DAC hubs with $3.5 billion in funding

DOCCS (Direct Ocean Capture with Storage)

DOCCS refers to the process of removing CO₂ directly from ocean water—where concentrations are ~150 times higher than air—and then permanently storing the captured CO₂ in deep geological formations, often offshore (e.g., basalt formations or saline aquifers). The ocean acts as a natural carbon sink, and DOCCS enhances that by reducing surface-level CO₂, prompting additional atmospheric CO₂ to be absorbed

Example Supplier: Equatic

Cost: $100-600/t

Current Landscape: Who’s Doing What?

The carbon removal landscape in the Middle East is still emerging, but notable actors—ranging from deep-tech startups to state-backed policy vehicles—have begun shaping a nascent ecosystem. Activity is clustered in Oman, the UAE, and Saudi Arabia, each leveraging distinct comparative advantages. However, overall deployment remains fragmented, with gaps in certification, MRV (monitoring, reporting, verification), and local supply chain capabilities.

1. Startups & CDR Suppliers

44.01 (Oman): One of the most advanced CDR startups in the region, 44.01 injects captured CO₂ into peridotite rock formations, where it rapidly mineralizes into stone. The company has received global recognition, including funding from Breakthrough Energy and Amazon’s Climate Pledge Fund, and has active partnerships with Omani ministries. Currently it partners with local stakeholders such as ADNOC, Masdar, and Fujairah Natural Resources Corporation for its pilot project in UAE.

Blue Carbon (UAE): As the UAE’s leading nature-based carbon project developer, Blue Carbon spearheads large-scale mangrove restoration and coastal ecosystem initiatives.

Climeworks (Switzerland): Signed an MoU with KAPSARC to jointly explore and advance DAC deployment in Saudi Arabia.

Emiratis CO2 (UAE): Inactive project. Participated in ADNOC’s global Decarbonization Technology Challenge.

2. Industrial Partners

ADNOC: UAE’s national oil company is positioning itself as a regional carbon management leader through partnerships with 44.01, Occidental, Carbon Clean, and LanzaTech, while piloting DAC and CCUS across its industrial footprint.

ADNOC x 44.01: Partnered with 44.01, Masdar, and FNRC on a successful carbon mineralization pilot in Fujairah.

ADNOC x Oxy: Conducting a joint DAC feasibility study with Occidental for a 1 mtpa facility connected to CO₂ injection wells in saline aquifers.

Aramco: Saudi Aramco is investing in DAC (e.g., CarbonCapture Inc.), CCUS hubs, and CO₂-to-hydrogen initiatives, aligning with its strategy to commercialize low-carbon technologies while offsetting industrial emissions.

Aramco x Siemens: Launched the Kingdom’s first CO2 Direct Air Capture test unit, capable of removing 12 tons of carbon dioxide per year from the atmosphere. Pilot plant was established with Siemens Energy to assess commercial scale-up of emissions-reduction technologies.

Siemens Energy: Partnered with Aramco to test and scale DAC units tailored for the Gulf climate, aiming to accelerate next-generation CO₂ capture materials.

Occidental: Partnered with ADNOC on a 1 mtpa CO₂ DAC facility feasibility study, connected to CO₂ injection wells in saline aquifers, in the UAE and jointly exploring broader regional storage hubs as part of its 1PointFive platform expansion.

3. Governmental Entities & National Research Centers

Ministry of Energy (KSA): Steering national CCUS and DAC strategy, with oversight over partnerships like KAPSARC x Climeworks.

Ministry of Climate Change and Environment (UAE): Plays a central role in integrating carbon removal into national strategies, while supporting innovation via platforms like ALTÉRRA and clean-tech policy roadmaps.

Ministry of Energy and Minerals (Oman): A key supporter of 44.01, Oman’s energy ministry is embedding CDR into its energy transition agenda, with a focus on geology-based solutions like mineralization.

KAPSARC (KSA): The Saudi energy think tank contributes research on CCUS, DAC, and carbon markets, supporting evidence-based policymaking and system-level modeling for durable CDR.

KAPSARC x Climeworks: Partnered with Climeworks to explore DAC applications under the Saudi Green Initiative.

Masdar (UAE): Through clean energy investments and platforms like The Catalyst, Masdar supports early-stage CDR innovation and is increasingly engaged in CCUS and hydrogen-carbon linkages.

Masdar x 44.01: Partnered with 44.01 on mineralization demonstration in Fujairah.

Saudi Green Initiative: A national Initiative launched to reduce emissions, increase green cover, and position Saudi Arabia as a leader in climate action.

RVCMC (KSA): Saudi Arabia’s dedicated carbon market authority, co-founded by PIF and Tadawul Group, aiming to position the Kingdom as a regional hub for high-integrity carbon crediting—including removals—by developing standards, registries, and structured market mechanisms. Currently, the focus remains on avoidance and reduction offsets rather than durable CDR procurement.

4. Academic Institutions

KAUST (KSA): Conducts cutting-edge research on carbon removal.

Sultan Qaboos University (Oman): Collaborates on mineralization R&D, supporting projects like 44.01 with geological studies and CO₂-rock interaction science.

Khalifa University (UAE): Focuses on carbon capture, clean fuels, and CDR-enabling technologies, with labs and RICH (Research and Innovation Center on CO₂ and Hydrogen) supporting partnerships with ADNOC and clean-tech accelerators.

5. Private Investors / Buyers

Shorooq Capital: A leading early-stage venture capital firm in the Middle East, Shorooq has shown growing interest in climate-aligned investments, particularly in green infrastructure and sustainable tech across the region.

IDO Investments (Oman): The investment arm of Oman Investment Authority, IDO backs high-impact startups and was an early investor in 44.01, supporting climate tech solutions with strategic value for Oman’s decarbonization goals.

Jasoor Ventures (KSA): A venture platform aligned with Saudi Arabia’s strategic priorities, Jasoor is increasingly active in clean energy, industrial decarbonization.

VentureSouq (UAE): A MENA-based VC with a dedicated ClimateTech fund, VentureSouq supports early-stage startups focused on circular economy and climate resilience.

ADNOC & Aramco: The two Gulf energy giants act as both buyers and investors in the carbon removal space, leveraging their financial strength and infrastructure to support global and regional CDR deployment.

Mubadala (UAE): In 2022, Mubadala acquired a strategic stake in AirCarbon Exchange (ACX), the first fully regulated carbon trading exchange and carbon clearing house in Abu Dhabi.

6. Non-Profits & International Organizations

UICCA (UAE Independent Climate Change Accelerators): Supports ecosystem building for climate innovation, including forums, pilot platforms, and advocacy for emerging technologies.

The Catalyst (Masdar + BP): The UAE’s first climate-tech accelerator, funding and mentoring startups in energy, circular economy, and early carbon removal sectors.

Hub71 (Abu Dhabi): A national innovation hub providing infrastructure and venture support to deep-tech companies—including those in energy transition, circular economy, and climate AI.

Nexus Climate (UAE): A regional platform connecting Middle East capital and resources with global climate projects and startups.

7. Platforms

AirCarbon Exchange (ACX), launched in Abu Dhabi in 2022 as the first fully regulated carbon trading exchange and carbon clearing house in Abu Dhabi, is closing its operations just one year after launch. ACX was a global environmental commodities exchange which allows corporations to finance and trade such commodities in a similar way to conventional financial assets.

Carbonmark (UAE): Carbonmark is a cutting-edge platform that connects environmental markets to the global economy. By employing blockchain infrastructure, Carbonmark facilitates the flow of environmental assets, ensuring transparent pricing, efficient settlements, and increased market confidence.

What’s Missing: Gaps in the Middle East CDR Ecosystem

Despite early momentum, the carbon removal ecosystem in the Middle East remains fragmented and underdeveloped. To unlock scalable, high-durability CDR, these foundational gaps should be addressed:

1. Lack of Deployable Technologies and Local Innovation Capacity

The region has limited local technological capacity in durable CDR, with most solutions still imported or in pilot phases. There is a need to cultivate localized innovation ecosystems through:

Academic–industry partnerships to accelerate R&D and adaptation of global technologies, such as RICH (Khalifa University) supporting scalable and commercializable technologies to deploy.

Incentives and soft landing programs to attract international CDR startups and innovators.

Regional R&D grants and accelerators focused on DAC, mineralization, and hybrid systems suited to Gulf geographies.

2. Lack of Bankable and Certifiable Projects

Beyond the tech, the region also suffers from a near-total absence of actual CDR project development. Few players have the technical expertise or institutional support to design, certify, and finance projects under global standards. Closing this pipeline gap requires:

Industrial partnerships (with CDR suppliers) to embed CDR into existing supply chains and repurpose legacy infrastructure (e.g., CO₂ pipelines, desalination brine).

Blended finance instruments to de-risk early-stage deployment and attract private capital.

Technical assistance to train developers and verifiers in MRV, certification, and registry engagement.

3. Lack of CDR-Specific Incentives Regulatory Frameworks

No GCC country currently has a dedicated policy framework or incentive structure for durable carbon removal. While national net-zero strategies mention emissions reductions and offsets, they lack concrete targets, procurement mandates, tax credits, or price signals specific to engineered CDR solutions.

In contrast, global peers are advancing rapidly:

The U.S. supports CDR through 45Q tax credits, Department of Energy grants, and multi-billion-dollar hubs.

The EU is developing a Carbon Removal Certification Framework (CRCF) and channeling funding through the Innovation Fund to support scale-up and market entry.

4. Weak and Unstructured Demand Signals

Corporate and sovereign buyers have not yet issued forward purchase commitments or formalized durable CDR procurement strategies. While the RVCMC has made progress in voluntary carbon market (VCM) transactions, its focus remains on avoidance credits. Durable CDR remains outside institutional procurement pathways.

Conclusion

While the Middle East’s carbon removal landscape is beginning to take shape, much remains to be done—from incentivizing suppliers to catalyzing project development and demand. Yet with emerging stakeholders and growing interest, the foundation for a regional CDR ecosystem is being laid. In the next articles of this series, we will explore specific CDR pathways, assessing their relevance, challenges, and potential to scale across the region.

Author’s Word: As I continue researching and documenting the evolving carbon removal landscape in the Middle East, I’m always open to learning from others. If you’re working in this space, curious about it, or simply want to exchange thoughts, I’d genuinely love to connect and have a conversation. Your insights could help shape the next chapters of this series.

Sources

Given the email length constraints, I will only mention the institute I took for reference.

Projects & Collaborations: Climeworks, ANDOC, ACX, FastCompany, 44.01.

CDR Methods & Roadmap: RMI, CarbonGap, CDR.FYI, State of CDR, BeZero, BCG, Roland Berger.

CDR in Middle East: SPGlobal, WeForum, Economy Middle East, CATF, CDR.FYI, MEI.